Business inventory capital asset classification presents a nuanced area within accounting and financial management. Understanding the distinctions between inventory treated as a current asset versus a capital asset is crucial for accurate financial reporting, tax compliance, and effective business decision-making. This exploration delves into the complexities of inventory valuation methods, their impact on reported capital asset values, and the strategic implications for inventory management and risk mitigation.

This discussion will cover the accounting treatment of inventory, exploring the conditions under which inventory might be classified as a capital asset. We will examine various inventory valuation methods (FIFO, LIFO, weighted average) and their effects on financial reporting. Furthermore, we will analyze best practices in inventory management to optimize capital asset utilization and explore the tax implications of different classifications.

Defining Business Inventory as a Capital Asset

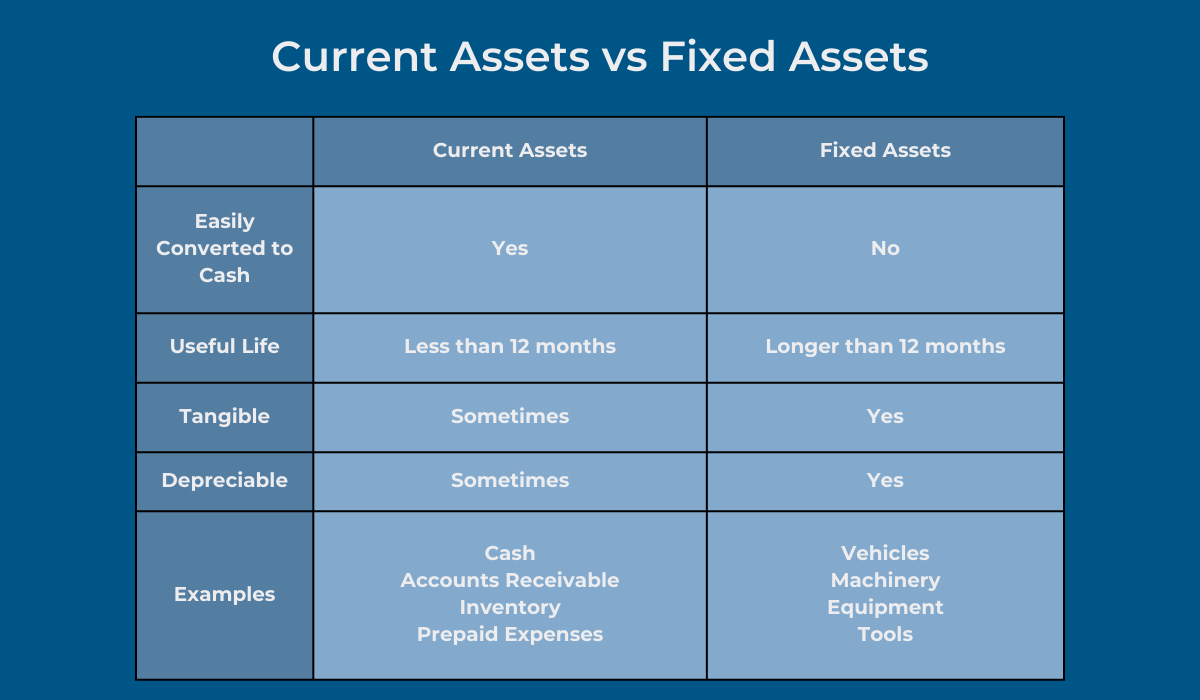

Inventory is typically treated as a current asset on a company’s balance sheet, reflecting its intended sale within the normal operating cycle. However, under specific circumstances, certain inventory items can be classified as capital assets. This distinction significantly impacts accounting treatment, particularly concerning depreciation and valuation methods.

Accounting Treatment of Inventory: Current vs. Capital Asset

The primary difference lies in the intended use. Current assets, like most inventory, are held for sale in the ordinary course of business. They are valued at the lower of cost or market value and are not depreciated. Capital assets, on the other hand, are held for use in the business for a period exceeding one year and are subject to depreciation to reflect their decline in value over time.

The choice between these classifications directly impacts a company’s financial statements and tax liabilities.

Conditions for Inventory Classification as a Capital Asset

Inventory is rarely classified as a capital asset. The most common scenario involves inventory items with a long lifespan and intended use within the business rather than for immediate resale. This could occur when a company holds specialized equipment or materials that are integral to its operations but not directly sold as products. Another condition might involve inventory items that have become obsolete or are no longer suitable for sale but still hold some residual value for internal use.

The crucial factor is the intent of the business regarding the item’s use.

Examples of Inventory Items Considered Capital Assets

Consider a manufacturing company that holds a specialized, highly customized machine used in its production process. While technically part of its inventory, its long-term use and integral role in production justify its classification as a capital asset. Similarly, a large quantity of rare earth elements purchased for a specific long-term project, rather than for immediate resale, could be classified as a capital asset.

The key is that these items are not intended for sale in the ordinary course of business, but rather for long-term use within the company’s operations.

Comparison of Accounting Methods for Current and Capital Assets

| Feature | Current Asset (Inventory) | Capital Asset |

|---|---|---|

| Valuation | Lower of cost or market value | Historical cost, less accumulated depreciation |

| Depreciation | Not applicable | Applicable (straight-line, declining balance, etc.) |

| Accounting Method | FIFO, LIFO, Weighted-Average Cost | Cost allocation methods |

| Balance Sheet Presentation | Current Assets | Property, Plant, and Equipment (PP&E) |

Impact of Inventory Valuation on Capital Asset Reporting

Inventory valuation significantly impacts a company’s reported capital asset values. The choice of valuation method directly affects the cost of goods sold (COGS) and, consequently, the reported net income and the value of inventory shown on the balance sheet. This, in turn, influences key financial ratios and the overall perception of the company’s financial health. Different valuation methods lead to different reported capital asset values, making a thorough understanding crucial for accurate financial reporting and decision-making.

Inventory Valuation Methods and Their Impact

Several methods exist for valuing inventory, each with its own implications for capital asset reporting. The most common are First-In, First-Out (FIFO), Last-In, First-Out (LIFO), and Weighted-Average Cost. FIFO assumes that the oldest inventory items are sold first, leaving the newest items in ending inventory. LIFO assumes the opposite—the newest items are sold first. The weighted-average cost method calculates a weighted average cost for all inventory items during a period.

In periods of rising prices, FIFO generally results in higher net income and higher inventory values on the balance sheet compared to LIFO. Conversely, LIFO produces lower net income and lower inventory values during inflationary periods. The weighted-average method falls somewhere between FIFO and LIFO, offering a more smoothed-out representation of inventory costs. The choice of method affects the reported cost of goods sold and, consequently, the net income.

This directly impacts the company’s overall financial position and the valuation of its capital assets, as inventory is often a significant component of a company’s total assets.

Inventory Write-Downs and Capital Asset Valuation

Inventory write-downs occur when the market value of inventory falls below its carrying cost. This is often due to obsolescence, damage, or market price fluctuations. When a write-down happens, the carrying value of the inventory is reduced, which directly impacts the reported value of total assets, including capital assets. This reduction is recognized as an expense on the income statement, lowering net income and consequently affecting various financial ratios.

The magnitude of the write-down’s impact on capital asset valuation depends on the proportion of inventory to the company’s total capital assets. A significant inventory write-down for a company with a large inventory holding can materially affect its reported capital asset value.

Impact of Valuation Methods on Financial Ratios

Different inventory valuation methods significantly influence several key financial ratios. For instance, the return on assets (ROA) ratio, calculated as net income divided by total assets, will vary depending on the inventory valuation method used. Similarly, the inventory turnover ratio, which measures how efficiently a company manages its inventory, will also be affected. FIFO generally leads to higher ROA and inventory turnover ratios during periods of rising prices compared to LIFO.

These differences in financial ratios can impact investor perceptions of a company’s profitability and efficiency, highlighting the importance of understanding the chosen inventory valuation method when analyzing financial statements. The current ratio (current assets/current liabilities) is also influenced, as inventory forms a significant part of current assets.

Hypothetical Scenario: Impact of Inventory Valuation on Capital Asset Position

Consider a company, “Tech Gadgets Inc.”, that manufactures and sells electronic devices. At the end of the year, they have 1000 units of their flagship product in inventory. The cost of these units varied throughout the year due to fluctuating raw material prices. Using FIFO, the cost of goods sold is calculated based on the cost of the first 1000 units purchased, resulting in a higher net income and higher reported inventory value.

Using LIFO, the cost of goods sold is calculated based on the cost of the last 1000 units purchased, resulting in a lower net income and lower reported inventory value. Let’s assume the difference in reported net income between FIFO and LIFO is $50,000, and the inventory value difference is $25,000. This difference directly impacts Tech Gadgets Inc.’s reported total assets and consequently its ROA, current ratio, and other financial ratios.

This scenario demonstrates how the choice of inventory valuation method can significantly influence a company’s reported capital asset position and its overall financial picture.

Inventory Management Strategies and Capital Asset Optimization

Effective inventory management is crucial for optimizing the return on capital assets tied up in inventory. Minimizing storage costs, reducing obsolescence, and ensuring timely availability of goods all contribute to a healthier bottom line and improved capital asset utilization. This section will explore best practices, key performance indicators, and the impact of specific strategies like Just-in-Time (JIT) inventory management.

Best Practices for Inventory Management

Implementing robust inventory management requires a multi-faceted approach. Successful strategies focus on accurate forecasting, efficient ordering processes, and diligent tracking of stock levels. This involves utilizing technology to streamline operations and gain real-time visibility into inventory. Furthermore, regular stock audits help to identify discrepancies and ensure data accuracy, preventing costly errors in financial reporting and asset valuation.

Finally, a strong relationship with suppliers is vital for ensuring timely delivery and preventing stockouts.

Key Performance Indicators (KPIs) for Inventory Management

Several key performance indicators provide insights into the efficiency of inventory management and its impact on capital assets. These metrics help businesses track their progress and identify areas for improvement.

- Inventory Turnover Ratio: This ratio (Cost of Goods Sold / Average Inventory) measures how efficiently inventory is used. A higher ratio generally indicates better inventory management and a quicker return on invested capital.

- Days Sales of Inventory (DSI): This metric (Average Inventory / Cost of Goods Sold)

– 365) shows the number of days it takes to sell the average inventory. A lower DSI signifies efficient inventory management and reduced capital tied up in stock. - Holding Cost Percentage: This represents the percentage of inventory value dedicated to storage, insurance, taxes, and obsolescence. Lowering this percentage directly improves profitability and capital asset utilization.

- Stockout Rate: This KPI tracks the percentage of orders that cannot be fulfilled due to insufficient inventory. Reducing stockouts minimizes lost sales and maintains customer satisfaction, indirectly improving capital asset efficiency by ensuring sales are not lost due to lack of stock.

Impact of Just-in-Time (JIT) Inventory Management on Capital Asset Structure, Business inventory capital asset

Just-in-Time (JIT) inventory management significantly impacts a business’s capital asset structure. By minimizing inventory holding, JIT frees up capital that would otherwise be tied up in stock. This capital can then be reinvested into other areas of the business, such as research and development, marketing, or expansion. However, JIT requires precise forecasting and reliable supplier relationships. A disruption in the supply chain can severely impact production and sales, highlighting the risks associated with this strategy.

For example, a company using JIT for manufacturing components might experience significant production delays and financial losses if a key supplier experiences unforeseen issues. This risk must be carefully weighed against the potential benefits of reduced capital investment.

Implementing a Robust Inventory Management System

Implementing a robust inventory management system requires a structured approach. This involves a step-by-step process to ensure successful integration and maximize efficiency.

- Needs Assessment: Begin by identifying the specific needs and challenges of the business. This involves analyzing current inventory processes, identifying pain points, and defining the goals of the new system.

- System Selection: Choose an inventory management system that aligns with the business’s requirements. This could range from a simple spreadsheet to a sophisticated enterprise resource planning (ERP) system.

- Data Migration: Accurately transfer existing inventory data into the new system. This step requires careful planning and validation to ensure data integrity.

- Training and Implementation: Provide thorough training to employees on how to use the new system. This is crucial for successful adoption and maximizing the system’s benefits.

- Monitoring and Optimization: Continuously monitor the system’s performance using the KPIs mentioned earlier. Regularly review and adjust the system to optimize its efficiency and adapt to changing business needs.

Financial Reporting and Disclosure of Inventory as a Capital Asset: Business Inventory Capital Asset

Properly reporting inventory, especially when classified as a capital asset, is crucial for accurate financial statement presentation and compliance with accounting standards. Misclassifications can lead to significant distortions in reported financial position and performance. This section details the required disclosures and the implications of incorrect classification.

Required Disclosures of Inventory as a Capital Asset

Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS) typically do not classify inventory as a capital asset. Inventory is considered a current asset, reflecting its intended sale or consumption within the normal operating cycle. However, in certain limited circumstances, such as with certain types of agricultural products or artwork held for appreciation, an argument could be made for classifying a subset of inventory as a long-term asset.

If such a classification is made, specific disclosures are necessary. These disclosures should clearly explain the rationale for the classification, the valuation method used, and any associated risks. The disclosure should include a detailed breakdown of the inventory items classified as capital assets, including their individual cost basis and any accumulated depreciation or impairment losses. This level of transparency ensures that financial statement users understand the nature and value of these assets.

Implications of Misclassifying Inventory as a Capital Asset

Misclassifying inventory as a capital asset has significant implications for financial reporting and compliance. Incorrect classification distorts the balance sheet, overstating long-term assets and understating current assets. This misrepresentation affects key financial ratios, potentially misleading investors and creditors. For instance, the current ratio (current assets/current liabilities), a key measure of short-term liquidity, would be artificially inflated. Furthermore, the income statement will be affected, as the depreciation of the misclassified inventory will be improperly recognized, impacting reported net income.

This can lead to penalties from regulatory bodies for non-compliance with accounting standards. In extreme cases, it can even lead to legal action from stakeholders who have made decisions based on the inaccurate financial information.

Presentation of Inventory Information in Financial Reports

When inventory is classified as a capital asset (a rare occurrence under standard accounting practices), its presentation in financial reports requires meticulous attention to detail. The financial statements should clearly distinguish between inventory treated as a current asset and any inventory classified as a capital asset. A separate line item within the balance sheet should be dedicated to inventory classified as a capital asset, with a corresponding disclosure in the notes explaining the rationale for this unusual classification.

The valuation method used (e.g., cost model, fair value model) should be explicitly stated, along with any adjustments made for depreciation, impairment, or other valuation allowances. Any significant changes in accounting policies related to the classification or valuation of this inventory should also be disclosed.

Sample Financial Statement Section

The following table provides a sample section of a balance sheet showing the proper reporting of inventory classified as a capital asset. Note that this scenario is exceptional and requires robust justification.

| Asset | Amount | Asset | Amount |

|---|---|---|---|

| Current Assets: | Long-Term Assets: | ||

| Inventory (Current) | $1,000,000 | Inventory (Capital Asset) | $500,000 |

| Other Current Assets | $500,000 | Accumulated Depreciation – Inventory | ($100,000) |

| Total Current Assets | $1,500,000 | Net Inventory (Capital Asset) | $400,000 |

Notes to the Financial Statements:

Note 1: Inventory classified as a capital asset represents a collection of rare antique furniture held for appreciation and eventual sale. The inventory is valued using the cost model, less accumulated depreciation. Depreciation is calculated using the straight-line method over the estimated useful life of each item. Impairment testing is performed annually.

Note 2: Management believes that the classification of this specific inventory as a capital asset is appropriate given its unique characteristics and the intention to hold it for appreciation rather than for immediate sale in the ordinary course of business. This classification is consistent with the company’s long-term investment strategy.

Tax Implications of Inventory Treated as a Capital Asset

Treating inventory as a capital asset, rather than the typical operating expense, significantly alters a company’s tax liability. This misclassification can lead to unexpected and potentially substantial tax consequences, stemming primarily from the differences in how capital assets and inventory are depreciated and taxed upon sale. Understanding these implications is crucial for accurate financial reporting and tax compliance.The primary tax implication of incorrectly classifying inventory as a capital asset lies in the timing and method of recognizing gains and losses.

Inventory is typically expensed when sold, directly impacting the cost of goods sold and thus the taxable income. Conversely, a capital asset’s sale triggers a capital gain or loss, taxed at different rates than ordinary income, and often subject to depreciation deductions over its useful life. This difference can result in either a higher or lower tax burden depending on various factors, including the asset’s holding period, the applicable tax rates, and the amount of depreciation claimed.

Depreciation of Inventory Treated as a Capital Asset

If inventory is mistakenly classified as a capital asset, depreciation deductions may be claimed. However, this is generally inappropriate for inventory items intended for sale in the ordinary course of business. Depreciation applies to assets with a useful life extending beyond one year, and is intended to recover the cost of the asset over its productive life.

Inventory, by its nature, is typically consumed or sold within a short period. Claiming depreciation on inventory could lead to an audit and potential penalties. The allowable depreciation methods (straight-line, declining balance, etc.) further complicate the calculation and increase the risk of error. For example, a company mistakenly depreciating its raw materials over several years would inflate its deductions in the early years and understate them later, potentially leading to discrepancies in tax filings.

Capital Gains Tax on Inventory Sale

When inventory, incorrectly classified as a capital asset, is sold, any profit is treated as a capital gain. The tax rate on capital gains generally differs from the ordinary income tax rate, often being lower for long-term capital gains (assets held for more than one year). However, this seemingly advantageous treatment can be misleading. The tax savings from a lower capital gains rate might be offset by the inability to deduct the cost of goods sold, leading to a higher overall tax burden compared to the proper treatment of inventory as an operating expense.

For instance, if a company sells inventory with a cost basis of $10,000 for $20,000, the proper treatment would recognize a $10,000 profit as ordinary income. If treated as a capital asset, the same $10,000 profit would be taxed at the capital gains rate, but the cost basis would not be deductible, leading to a potential difference in tax liability depending on the applicable rates.

Tax Treatment Comparison Across Jurisdictions

The specific tax implications of misclassifying inventory vary across different tax jurisdictions. Some jurisdictions may have stricter rules regarding the definition of capital assets and inventory, leading to higher penalties for incorrect classification. Others might offer more lenient treatment, but the fundamental difference in tax rates between ordinary income and capital gains remains a consistent factor influencing the overall tax liability.

International tax treaties and transfer pricing regulations also add layers of complexity when dealing with inventory across borders, potentially exacerbating the consequences of incorrect classification. A thorough understanding of the specific rules in each relevant jurisdiction is therefore essential.

Scenario: Tax Advantages and Disadvantages

Let’s consider a small business that manufactures and sells handcrafted furniture. They mistakenly classify their lumber inventory as a capital asset, depreciating it over five years using the straight-line method. In the first year, they claim depreciation on $50,000 worth of lumber, reducing their taxable income. However, when they sell the finished furniture made from this lumber, the profit is treated as a capital gain, potentially at a lower tax rate.

However, if they had correctly treated the lumber as inventory, the cost of the lumber would have been deducted as part of the cost of goods sold, potentially resulting in a lower overall tax liability. The net tax effect depends on the applicable tax rates for ordinary income and capital gains, as well as the amount of depreciation claimed.

The scenario highlights the complexity of the issue and the potential for either tax advantages or disadvantages depending on the specific circumstances.

Risk Management and Inventory as a Capital Asset

Classifying inventory as a capital asset significantly alters the risk profile of a business. While offering potential tax advantages, this approach necessitates a robust risk management strategy to address the unique challenges presented. Failure to adequately manage these risks could lead to substantial financial losses.Treating inventory as a capital asset exposes the business to different risks compared to the traditional approach of expensing it.

These risks stem primarily from the longer holding period, increased valuation complexities, and the potential for significant losses if the inventory’s value depreciates or becomes obsolete. Effective mitigation strategies are crucial to protect the business’s financial health.

Potential Risks Associated with Classifying Inventory as a Capital Asset

The decision to classify inventory as a capital asset introduces several potential risks. These risks are not trivial and require careful consideration and proactive mitigation strategies. Failing to adequately address these risks can lead to significant financial losses and negatively impact the business’s overall performance. For instance, the longer holding period associated with capital assets increases the likelihood of obsolescence, damage, or theft, all of which can lead to substantial write-downs or losses.

Furthermore, the complexities associated with valuing capital assets, including the potential for disputes with tax authorities, add another layer of risk.

Strategies for Mitigating Risks Related to Inventory Obsolescence, Damage, and Theft

Effective inventory management is paramount when treating inventory as a capital asset. Proactive strategies can significantly reduce the impact of obsolescence, damage, and theft. Implementing robust inventory tracking systems, employing appropriate storage and security measures, and regularly reviewing inventory levels are essential. For obsolescence, forecasting demand accurately and diversifying inventory holdings can help minimize losses. To mitigate damage, proper handling procedures and appropriate storage conditions are necessary.

Theft prevention involves security systems, employee training, and regular audits.

Examples of Insurance Coverage Appropriate for Inventory Classified as a Capital Asset

Appropriate insurance coverage is critical for protecting the value of inventory classified as a capital asset. Businesses should consider comprehensive insurance policies that cover a range of potential losses, including:

- Inventory insurance: This covers losses due to fire, theft, vandalism, and other unforeseen events.

- Business interruption insurance: This compensates for lost income due to disruptions caused by damage to or loss of inventory.

- Liability insurance: This protects against claims of damage or injury caused by the inventory.

The specific coverage required will depend on the nature of the inventory, its value, and the business’s risk profile. It is advisable to consult with an insurance professional to determine the appropriate level of coverage.

Risk Management Checklist for Inventory Treated as a Capital Asset

A comprehensive checklist ensures consistent risk management practices. Regular reviews and updates are crucial to adapt to changing circumstances and emerging threats.

- Regular inventory audits to identify obsolete or damaged items.

- Implementation of a robust inventory tracking system with real-time visibility.

- Secure storage facilities with appropriate environmental controls (temperature, humidity).

- Employee training on proper inventory handling and security procedures.

- Regular security assessments and upgrades to security systems (alarms, cameras).

- Insurance policy review and updates to ensure adequate coverage.

- Development of contingency plans for handling inventory losses or damage.

- Periodic review of inventory valuation methods and compliance with relevant accounting standards.

- Documentation of all inventory-related transactions and procedures.

- Regular reconciliation of physical inventory with accounting records.

Closing Notes

Successfully navigating the complexities of business inventory capital asset management requires a thorough understanding of accounting principles, tax regulations, and effective inventory control strategies. By accurately classifying inventory, employing appropriate valuation methods, and implementing robust risk management procedures, businesses can ensure compliance, optimize financial reporting, and maximize the return on their invested capital. Careful consideration of these factors is essential for long-term financial health and sustainable growth.

Questions Often Asked

What are the potential penalties for misclassifying inventory?

Misclassifying inventory can lead to inaccurate financial statements, resulting in penalties from regulatory bodies, potential legal issues, and misinformed business decisions.

How often should inventory be reviewed for capital asset classification?

Regular reviews, ideally annually or more frequently for rapidly changing inventories, are recommended to ensure accurate classification and valuation.

Can all types of inventory be considered capital assets?

No, typically only inventory items with a long lifespan and significant value, and intended for long-term use rather than immediate sale, qualify for capital asset classification.

What insurance is suitable for inventory classified as a capital asset?

Appropriate insurance coverage would include comprehensive business property insurance, potentially with specific endorsements for valuable or specialized inventory items.