Business inventory fiscal year tax presents a significant challenge for many businesses. Understanding the intricacies of inventory valuation methods (FIFO, LIFO, weighted-average cost), their impact on taxable income, and the implications for year-end reporting is crucial for tax compliance and optimization. This guide delves into these complexities, providing practical strategies for effective inventory management and minimizing tax liabilities.

We’ll explore the Uniform Capitalization Rules (UNICAP), the process of inventory write-downs, and best practices to ensure accurate reporting and efficient cash flow.

Proper inventory management is not merely an accounting function; it’s a strategic tool for financial health. By accurately tracking inventory, businesses gain a clearer picture of their profitability, allowing for informed decision-making regarding pricing, purchasing, and overall business strategy. This understanding directly translates into reduced tax burdens and improved financial stability.

Inventory Valuation Methods for Tax Purposes

Choosing the right inventory valuation method is crucial for accurate financial reporting and minimizing your tax liability. Different methods impact how the cost of goods sold (COGS) is calculated, directly affecting your net income and ultimately, your tax burden. Understanding these methods is essential for businesses to make informed decisions.

Inventory Valuation Methods: FIFO, LIFO, and Weighted-Average Cost

Businesses can use several methods to value their inventory for tax purposes. The three most common are First-In, First-Out (FIFO), Last-In, First-Out (LIFO), and Weighted-Average Cost. The choice of method can significantly impact a company’s reported profits and taxes, particularly in times of fluctuating prices. Tax laws often dictate which methods are permissible, and the selection should be consistent from year to year unless there’s a justifiable reason for a change.

First-In, First-Out (FIFO)

FIFO assumes that the oldest inventory items are sold first. This means the cost of goods sold reflects the cost of the earliest acquired items. In periods of rising prices, FIFO results in a lower COGS and higher net income compared to other methods. This, in turn, leads to a higher tax liability. Conversely, in periods of falling prices, FIFO leads to a higher COGS and lower net income, resulting in a lower tax liability.

On the balance sheet, FIFO typically shows a higher inventory value, reflecting the current market prices of the most recently acquired goods.

Last-In, First-Out (LIFO)

LIFO assumes that the newest inventory items are sold first. Therefore, the cost of goods sold reflects the cost of the most recently acquired items. In periods of rising prices, LIFO results in a higher COGS and lower net income, leading to a lower tax liability. This is a significant advantage during inflationary periods. Conversely, in periods of falling prices, LIFO results in a lower COGS and higher net income, increasing the tax liability.

On the balance sheet, LIFO usually shows a lower inventory value, as it reflects the cost of older, potentially less valuable items. Note that LIFO is not permitted under International Financial Reporting Standards (IFRS).

Weighted-Average Cost

The weighted-average cost method assigns a weighted-average cost to each item in inventory. This average is calculated by dividing the total cost of goods available for sale by the total number of units available for sale. This method smooths out price fluctuations, resulting in a COGS that is less sensitive to price changes than FIFO or LIFO. The tax implications are somewhere between those of FIFO and LIFO, depending on the price trends.

The balance sheet reflects an inventory value that is a blend of older and newer costs.

Cost of Goods Sold (COGS) Calculation Examples

Let’s assume a company purchased the following inventory:

- January 1: 100 units @ $10/unit

- March 1: 150 units @ $12/unit

- June 1: 200 units @ $15/unit

They sold 300 units during the year. The COGS calculation for each method is shown below:

| Method | Calculation | COGS Result | Tax Impact |

|---|---|---|---|

| FIFO | (100 units

|

$3400 | Higher net income, higher tax liability |

| LIFO | (200 units

|

$4200 | Lower net income, lower tax liability |

| Weighted-Average | [(100*$10)+(150*$12)+(200*$15)] / (100+150+200) = $13.14 per unit; 300 units – $13.14 = $3942 | $3942 | Intermediate net income and tax liability |

Impact of Inventory on Fiscal Year-End Tax Reporting

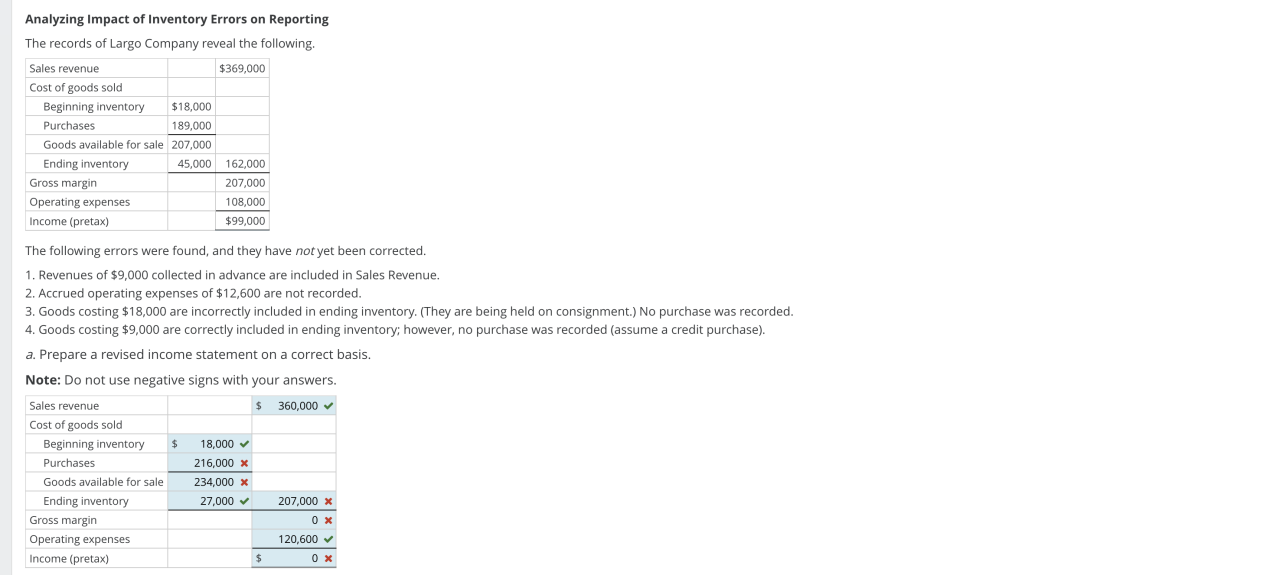

Accurate inventory accounting is crucial for accurate financial reporting and, consequently, for compliant tax filings. Miscalculations can lead to significant financial repercussions, impacting profitability and potentially resulting in penalties. The year-end inventory count is a critical component of this process, directly influencing the cost of goods sold (COGS) calculation, a key determinant of taxable income.Accurate inventory counts at fiscal year-end are paramount for tax compliance.

An accurate count directly impacts the calculation of cost of goods sold (COGS), a crucial deduction that reduces taxable income. Overstating inventory inflates COGS, understating taxable income and potentially leading to underpayment of taxes. Conversely, understating inventory deflates COGS, overstating taxable income and resulting in overpayment of taxes. Both scenarios can have serious consequences.

Potential Penalties for Inaccurate Inventory Reporting

Inaccurate inventory reporting can result in significant penalties from tax authorities. These penalties can vary depending on the jurisdiction and the severity of the inaccuracy, but generally include financial penalties, interest charges on underpaid taxes, and in severe cases, legal action. For instance, intentional misrepresentation of inventory values for tax evasion can lead to substantial fines and even criminal prosecution.

The IRS, for example, has a range of penalties for tax-related infractions, with penalties often increasing based on the amount of underpayment and whether the inaccuracy was intentional or due to negligence.

Adjusting Inventory Values for Obsolescence or Damage

Inventory items can become obsolete or damaged, reducing their value. Businesses must account for these losses to ensure accurate financial reporting. Obsolescence may occur due to technological advancements, changes in consumer demand, or simply the passage of time. Damage can result from various factors, including improper storage, handling, or transportation. To adjust for these losses, businesses typically use the lower of cost or market (LCM) method.

This method requires that inventory be valued at the lower of its original cost or its current market value, reflecting the impact of obsolescence or damage. For example, if a company has a batch of electronics that are now outdated due to a newer model, their value should be adjusted downwards to reflect their current market price, not their original purchase cost.

This adjustment reduces the value of inventory on the balance sheet and increases COGS, thereby lowering taxable income.

Checklist for Accurate Year-End Inventory Reporting

A comprehensive checklist is vital for ensuring accurate inventory reporting. This checklist should be followed diligently throughout the year, but especially in the lead-up to the fiscal year-end.

- Conduct a thorough physical inventory count, ideally using a standardized counting method and involving multiple personnel to minimize errors.

- Reconcile the physical count with inventory records to identify discrepancies and investigate the causes of any differences.

- Implement a robust inventory management system that tracks inventory levels in real-time, minimizing the risk of errors and providing an accurate basis for the year-end count.

- Document all adjustments made to inventory values, including those for obsolescence or damage, with supporting documentation.

- Review the inventory valuation method used for tax purposes, ensuring compliance with relevant tax regulations.

- Consult with a tax professional to ensure compliance with all relevant tax laws and regulations.

- Maintain detailed records of all inventory transactions throughout the year, including purchases, sales, and adjustments.

- Establish clear procedures for handling damaged or obsolete inventory, including methods for disposal or write-off.

Inventory Management and Tax Optimization Strategies

Effective inventory management is crucial for minimizing tax liabilities and maximizing profitability. By implementing robust systems and strategies, businesses can significantly reduce their tax burden and improve overall financial health. This section explores best practices for inventory management, potential tax deductions, and a step-by-step guide to implementing an effective system.

Best Practices for Inventory Management to Minimize Tax Liabilities, Business inventory fiscal year tax

Maintaining accurate inventory records is paramount for minimizing tax liabilities. This involves employing a reliable inventory tracking system, regularly conducting physical inventory counts to reconcile with recorded data, and implementing robust internal controls to prevent discrepancies. Adopting the First-In, First-Out (FIFO) or Last-In, First-Out (LIFO) methods for inventory valuation can significantly impact the cost of goods sold (COGS) and, consequently, taxable income.

Careful consideration of these methods and their tax implications is essential. Regularly reviewing inventory levels to avoid overstocking or stockouts helps optimize carrying costs and prevents losses due to obsolescence or spoilage.

Potential Tax Deductions Related to Inventory

Several deductions can reduce a business’s tax liability related to inventory. Storage costs, including rent, utilities, and insurance for warehouse space, are generally deductible expenses. Furthermore, businesses can deduct losses due to inventory obsolescence, damage, or spoilage. These losses should be properly documented and supported by evidence. Write-downs of inventory value to reflect market value or lower of cost or market (LCM) are also deductible, reducing taxable income.

Proper documentation is key to claiming these deductions.

Step-by-Step Guide for Implementing an Effective Inventory Management System for Tax Purposes

Implementing an effective inventory management system involves several key steps. First, select an appropriate inventory tracking method, whether manual or automated. Second, implement regular physical inventory counts to ensure accuracy and reconcile with recorded data. Third, establish clear procedures for receiving, storing, and issuing inventory. Fourth, maintain detailed records of all inventory transactions, including purchase orders, invoices, and sales receipts.

Fifth, periodically review inventory levels to identify slow-moving or obsolete items. Finally, reconcile inventory records with financial statements to ensure consistency. This systematic approach ensures compliance and accurate tax reporting.

How Proper Inventory Tracking Improves Cash Flow and Reduces Tax Burden

Proper inventory tracking directly impacts cash flow and reduces the tax burden. Accurate inventory data allows for better forecasting of sales and purchasing needs, optimizing cash flow by minimizing unnecessary inventory holding costs. Efficient inventory management minimizes waste from obsolescence or spoilage, directly impacting COGS and reducing taxable income. Accurate COGS calculations, resulting from proper inventory tracking, lead to a more precise determination of taxable income, minimizing potential tax penalties or audits.

Inventory Management Strategies: A Comparative Overview

| Strategy | Implementation | Benefits | Tax Implications |

|---|---|---|---|

| Regular Physical Inventory Counts | Conducting physical counts at least annually, or more frequently depending on business needs. | Improved accuracy of inventory records, reduced risk of discrepancies, better tax compliance. | More accurate COGS calculation, minimizing tax liabilities. |

| FIFO/LIFO Inventory Valuation | Choosing the appropriate method based on business circumstances and tax implications. | FIFO provides a more accurate reflection of current costs, while LIFO can reduce taxable income in inflationary environments. | Impacts COGS and net income, thus affecting the amount of taxes owed. LIFO is only permitted under certain conditions. |

| Just-in-Time (JIT) Inventory Management | Ordering inventory only when needed, minimizing storage costs. | Reduced storage costs, lower risk of obsolescence, improved cash flow. | Lower COGS, potentially leading to lower tax liability, but requires careful planning and execution to avoid stockouts. |

| ABC Analysis | Categorizing inventory items based on their value and consumption rate. | Prioritize inventory control efforts on high-value items, optimizing resource allocation. | More efficient inventory management, leading to improved accuracy in COGS calculation and better tax compliance. |

Tax Implications of Inventory Write-Downs and Obsolescence

Inventory write-downs, necessitated by obsolescence or damage, significantly impact a business’s financial statements and tax liability. Understanding the process and tax consequences is crucial for accurate financial reporting and tax compliance. This section details the procedures involved in writing down inventory and the resulting tax implications.

Process and Criteria for Writing Down Obsolete or Damaged Inventory

Determining the need for an inventory write-down involves a careful assessment of the inventory’s current market value compared to its original cost. If the market value falls below the cost, a write-down is necessary to reflect the inventory’s true value. This usually happens when inventory becomes obsolete due to technological advancements, changes in consumer demand, or damage rendering it unsaleable.

The write-down amount is the difference between the original cost and the net realizable value (NRV). NRV is the estimated selling price less any costs of completion, disposal, and transportation. Companies often use a variety of methods to determine NRV, including market analysis, expert appraisals, and internal assessments. For example, a clothing retailer might write down the value of last season’s out-of-fashion garments if they are unlikely to sell at their original cost.

Similarly, a food manufacturer might write down the value of damaged goods due to spoilage or improper storage.

Tax Implications of Inventory Write-Downs

Inventory write-downs are generally considered a deductible expense for tax purposes. This reduces the company’s taxable income, resulting in a lower tax liability. However, the specific tax treatment depends on the accounting method used (e.g., FIFO, LIFO). The timing of the deduction also plays a crucial role. The write-down is typically recognized in the year the obsolescence or damage is discovered, impacting that year’s tax return.

The amount of the write-down is directly subtracted from the cost of goods sold (COGS), effectively reducing the company’s taxable income. For example, if a company writes down $10,000 worth of obsolete inventory, its taxable income is reduced by $10,000, leading to a lower tax bill. It’s important to maintain accurate records supporting the write-down, including documentation of the obsolescence or damage, and the calculation of NRV.

Examples of Situations Requiring Inventory Write-Downs and Their Associated Tax Consequences

Several scenarios illustrate the need for inventory write-downs and their impact on taxes.

- Scenario 1: Technological Obsolescence: A technology company discovers that a significant portion of its inventory of computer components is obsolete due to the release of newer, faster components. The company writes down the inventory to its net realizable value, reducing its taxable income and tax liability for the year.

- Scenario 2: Damage: A food processing plant experiences a power outage, leading to spoilage of a large quantity of perishable goods. The damaged inventory is written down, reducing the company’s taxable income. The tax savings offset some of the financial losses due to spoilage.

- Scenario 3: Changes in Consumer Demand: A fashion retailer finds that a particular line of clothing is not selling well due to changing fashion trends. The unsold inventory is written down to its net realizable value, which is significantly lower than the original cost. This reduces the company’s taxable income for the year.

Comparison of Accounting Treatment and Tax Treatment of Inventory Write-Downs

The accounting treatment and tax treatment of inventory write-downs are generally aligned, but some differences can exist due to specific accounting standards and tax regulations.

- Accounting Treatment: Inventory write-downs are recorded as a reduction in the value of inventory on the balance sheet and as an expense on the income statement (reducing net income). Generally follows GAAP (Generally Accepted Accounting Principles) or IFRS (International Financial Reporting Standards).

- Tax Treatment: Inventory write-downs are generally deductible expenses, reducing taxable income. The deduction is usually taken in the year the obsolescence or damage is determined. Tax treatment follows the relevant tax code and regulations of the jurisdiction.

- Key Difference: While both accounting and tax treatments aim to reflect the true economic value of inventory, the specific methods used and the timing of recognition might differ slightly depending on the accounting method chosen (FIFO, LIFO) and tax regulations.

Inventory and the Uniform Capitalization Rules

The Uniform Capitalization Rules (UNICAP) significantly impact how businesses account for inventory costs for tax purposes. Understanding UNICAP is crucial for accurate tax reporting and minimizing potential liabilities. These rules dictate which costs must be capitalized as part of inventory, rather than expensed in the period they are incurred. Failure to comply with UNICAP can result in significant tax penalties.

Direct and Indirect Costs Under UNICAP

UNICAP classifies costs as either direct or indirect. Direct costs are those directly attributable to the production of goods. Indirect costs, conversely, are those related to production but not directly traceable to a specific product. Accurate categorization is paramount for correct inventory valuation. The precise definition of direct and indirect costs can be nuanced and depends on the specific industry and production processes.

Examples of Costs Included and Excluded from Inventory

Direct costs included under UNICAP typically encompass raw materials, direct labor, and manufacturing supplies directly used in the production process. For example, the cost of wood used in furniture manufacturing, the wages of carpenters assembling the furniture, and the cost of nails and glue are all considered direct costs. Indirect costs included under UNICAP can include factory overhead (rent, utilities, depreciation of factory equipment), and certain administrative and selling expenses, if directly related to the production process.

Conversely, costs like marketing expenses, research and development unrelated to a specific product, and general administrative expenses not directly tied to production are typically excluded from inventory costs under UNICAP.

Allocating Indirect Costs to Inventory Under UNICAP

Allocating indirect costs to inventory under UNICAP requires a systematic approach. Businesses typically use a method that reasonably reflects the relationship between indirect costs and the production of inventory. Common methods include allocation based on direct labor hours, machine hours, or square footage of production space. The chosen method should be consistently applied and documented.

For example, consider a furniture manufacturer with total indirect costs of $100,000 (factory rent, utilities, and depreciation) and 10,000 direct labor hours used in production. If a particular chair model requires 10 direct labor hours to produce, the allocated indirect cost for that chair would be ($100,000 / 10,000 hours)

– 10 hours = $10. This $10 would then be added to the direct costs of the chair to determine its total capitalized cost for inventory purposes.

The choice of allocation method is crucial and should be carefully considered to ensure accuracy and compliance.

Final Thoughts

Mastering the complexities of business inventory fiscal year tax requires a multifaceted approach. From understanding the nuances of inventory valuation methods and their impact on taxable income to implementing effective inventory management systems and utilizing available tax optimization strategies, businesses can significantly improve their financial performance. By adhering to best practices, accurately reporting inventory values, and staying informed about relevant tax regulations, companies can ensure compliance, minimize liabilities, and ultimately, thrive.

Commonly Asked Questions: Business Inventory Fiscal Year Tax

What are the penalties for inaccurate inventory reporting?

Penalties for inaccurate inventory reporting can vary depending on the jurisdiction and the severity of the error, but they can include significant fines, interest charges, and even legal repercussions.

How often should a business perform inventory counts?

The frequency of inventory counts depends on the nature of the business and the type of inventory. Some businesses may conduct counts monthly, while others may do so quarterly or annually. Regular counts help ensure accuracy and identify potential issues early on.

Can I deduct the cost of obsolete inventory?

Yes, under certain circumstances, you can deduct the cost of obsolete inventory as a loss. This typically involves following specific accounting procedures and providing proper documentation to the tax authorities.

What is the difference between direct and indirect costs under UNICAP?

Direct costs are directly attributable to producing the inventory (e.g., raw materials), while indirect costs are those that support production but aren’t directly tied to a specific item (e.g., factory rent).