Business inventory for new bussiness partnership – Business inventory for new business partnerships is a critical aspect often overlooked during the initial excitement of a new venture. Successfully navigating the complexities of inventory management from the outset is crucial for the long-term health and profitability of the partnership. This guide explores the essential steps involved in assessing, managing, and optimizing inventory, ensuring a solid foundation for shared success.

From initial inventory assessment and the selection of appropriate valuation methods (FIFO, LIFO, weighted average) to implementing effective inventory management systems (perpetual vs. periodic), this resource provides a comprehensive framework. We will delve into the legal and financial implications, including inventory ownership, liability allocation, and tax considerations. Furthermore, we’ll explore the benefits of technology integration, such as inventory management software and barcode scanning, to streamline processes and enhance efficiency.

Finally, we’ll address risk mitigation strategies to protect against inventory loss, damage, or obsolescence.

Initial Inventory Assessment for a New Business Partnership

A thorough inventory assessment is crucial before finalizing a business partnership. This process ensures transparency, establishes a baseline for future performance tracking, and prevents disputes regarding asset valuation. A comprehensive evaluation will contribute significantly to the success and stability of the new partnership.

Inventory Evaluation Checklist

Prior to forming a partnership, a detailed review of the existing inventory is paramount. This checklist will guide a systematic assessment:

- Item Identification: A complete list of all inventory items, including descriptions and unique identifiers (e.g., SKU numbers).

- Quantity on Hand: Accurate count of each item, noting any damaged or obsolete goods.

- Condition Assessment: Evaluation of the condition of each item (new, used, damaged, obsolete).

- Location Tracking: Precise location of inventory within the business premises (warehouse, store, etc.).

- Purchase Date and Cost: Documentation of the original purchase price and date for each item.

- Market Value Determination: Estimate of current market value for each item, considering factors like demand and condition.

- Storage Conditions: Assessment of storage conditions to identify potential risks (e.g., damage from humidity, temperature fluctuations).

- Insurance Coverage: Review of existing insurance policies to ensure adequate coverage for the inventory.

Inventory Valuation Methods Comparison

Different methods exist for valuing inventory, each impacting the financial statements differently. Choosing the appropriate method depends on the industry, accounting standards, and management objectives.

| Method | Description | Impact on Cost of Goods Sold (COGS) | Impact on Net Income |

|---|---|---|---|

| FIFO (First-In, First-Out) | Assumes that the oldest inventory is sold first. | Lower COGS during inflation, higher during deflation. | Higher net income during inflation, lower during deflation. |

| LIFO (Last-In, First-Out) | Assumes that the newest inventory is sold first. (Note: LIFO is not permitted under IFRS). | Higher COGS during inflation, lower during deflation. | Lower net income during inflation, higher during deflation. |

| Weighted Average Cost | Calculates the average cost of all inventory items. | COGS reflects the average cost of goods. | Net income reflects the average cost of goods. |

Importance of Accurate Inventory Records in a Partnership Agreement

Accurate inventory records are fundamental to a successful partnership. They provide a transparent basis for:* Profit and Loss Sharing: Accurate valuation ensures fair distribution of profits and losses among partners.

Financial Reporting

Reliable data for accurate financial statements, crucial for securing loans or attracting investors.

Tax Compliance

Correct inventory valuation is essential for accurate tax reporting and avoiding penalties.

Inventory Management

Efficient inventory control, preventing stockouts and minimizing waste.

Dispute Resolution

Clear records prevent disagreements regarding inventory ownership and value.

Physical Inventory Counting and Verification

A physical inventory count is essential to verify the accuracy of existing records. The process typically involves:

- Planning: Develop a detailed plan, including timelines, team assignments, and necessary equipment.

- Preparation: Gather necessary supplies such as counting sheets, barcode scanners, and potentially additional personnel.

- Counting: Systematically count all inventory items, ensuring accuracy and double-checking counts.

- Reconciliation: Compare the physical count with existing inventory records, identifying any discrepancies.

- Investigation: Investigate and resolve any significant discrepancies found during the reconciliation process.

- Documentation: Thoroughly document the entire process, including dates, counts, and any adjustments made.

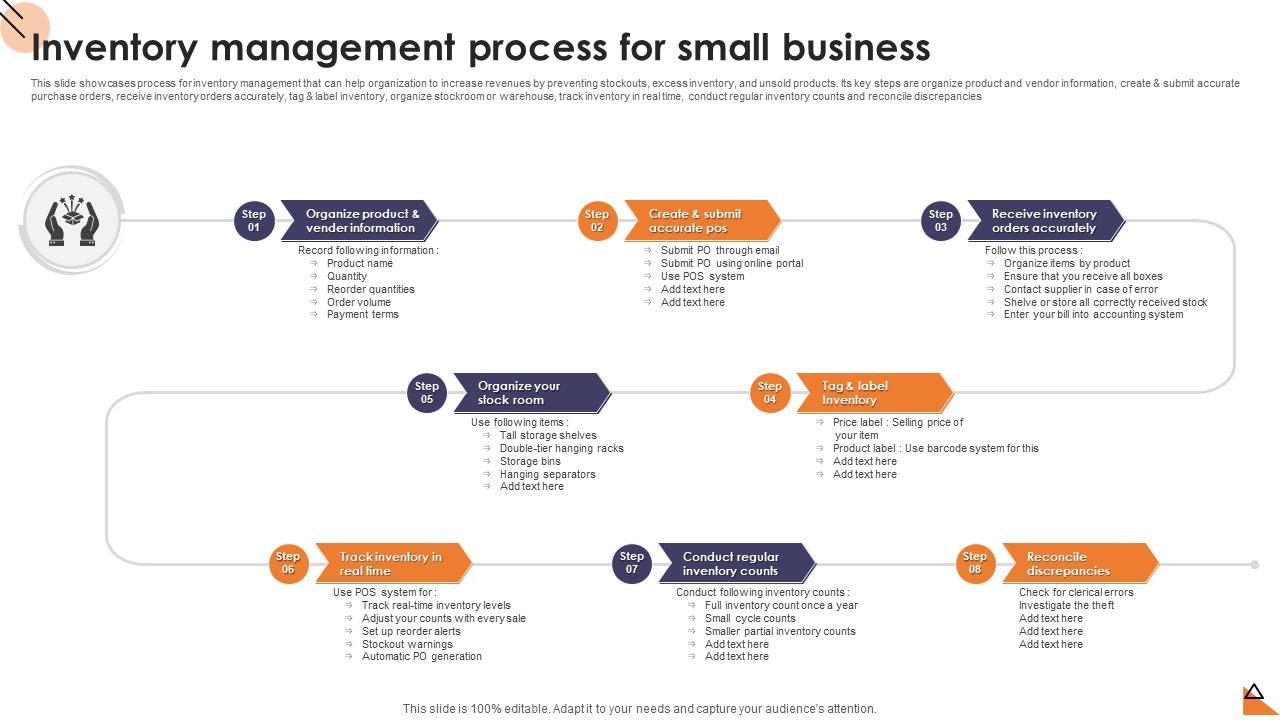

Inventory Management Strategies for the New Partnership

Effective inventory management is crucial for a new business partnership’s success. Maintaining optimal stock levels, minimizing waste, and accurately tracking inventory directly impact profitability and operational efficiency. Choosing the right system and implementing robust tracking methods are key to achieving these goals.

Inventory Management System Comparison: Perpetual vs. Periodic

Perpetual and periodic inventory systems represent two distinct approaches to tracking inventory. A perpetual system provides real-time inventory updates through continuous monitoring of stock levels. Each sale or purchase is recorded immediately, offering a constant, accurate view of available inventory. This system requires a more advanced technological infrastructure, often involving barcode scanners and inventory management software. Conversely, a periodic system relies on physical counts conducted at fixed intervals (e.g., monthly, quarterly).

While simpler to implement initially, it provides less immediate visibility into inventory levels and may lead to stock discrepancies if not managed carefully. The choice depends on factors such as the volume of transactions, budget, and the desired level of accuracy. A small business with lower transaction volumes might find a periodic system sufficient, while a larger operation with high turnover will benefit from the real-time insights of a perpetual system.

Implementing a Perpetual Inventory Management System

Implementing a perpetual system involves a structured approach. First, invest in appropriate inventory management software or a point-of-sale (POS) system with inventory tracking capabilities. Second, assign unique identification numbers (e.g., barcodes or SKUs) to each item in your inventory. Third, establish a standardized procedure for recording all inventory transactions (purchases, sales, returns, adjustments). This includes training employees on proper scanning and data entry practices.

Fourth, regularly reconcile the system’s inventory data with physical stock counts to identify and correct any discrepancies. Finally, monitor key performance indicators (KPIs) such as inventory turnover rate and stock-out rates to fine-tune the system’s effectiveness. For example, a local bakery might use a POS system with barcode scanning to track flour, sugar, and other ingredients, ensuring they always have sufficient supplies for baking while avoiding spoilage from overstocking.

Tracking Inventory Turnover Rates and Identifying Slow-Moving Items

Efficient inventory management requires monitoring inventory turnover rate, which measures how quickly inventory is sold and replenished. The formula is: Cost of Goods Sold / Average Inventory. A high turnover rate generally indicates strong sales and efficient inventory management. Conversely, a low turnover rate suggests slow-moving items that may require price adjustments or promotional strategies. To identify slow-moving items, analyze sales data over a specific period.

Items with consistently low sales figures relative to their stock levels are flagged as slow-moving. For example, a clothing store might track turnover rates for each clothing item, identifying slow-selling styles to adjust pricing or clear out inventory through sales.

Preventing Inventory Shrinkage and Loss

Inventory shrinkage refers to the unexplained loss of inventory due to theft, damage, spoilage, or errors. Implementing robust security measures is crucial to minimize this loss. This includes physical security measures such as locked storage areas and security cameras, as well as internal controls such as regular inventory counts and employee training on proper handling and storage procedures. Implementing a system of regular cycle counts—periodic checks of a portion of the inventory rather than a complete count—can also help to identify shrinkage early on.

For example, a hardware store might use security cameras and regular cycle counts to monitor inventory, promptly addressing any discrepancies and deterring potential theft. By employing these strategies, businesses can protect their assets and maintain accurate inventory records.

Legal and Financial Aspects of Inventory in a Partnership

Successfully managing inventory is crucial for any partnership’s profitability and longevity. However, the legal and financial implications of inventory ownership, valuation, and distribution are often overlooked. Understanding these aspects is vital for preventing disputes and ensuring the partnership’s financial health. This section details the key legal and financial considerations related to inventory within a business partnership.

Inventory Ownership and Liability in Partnership Agreements

A clearly defined partnership agreement is essential for outlining inventory ownership and liability. The agreement should specify how inventory is acquired, owned, and managed. For instance, it should clarify whether inventory is owned jointly by all partners or if individual partners have ownership stakes in specific inventory items. The agreement should also address liability for inventory loss or damage, including instances of theft, spoilage, or obsolescence.

Failure to address these issues in the partnership agreement can lead to significant disagreements and potential legal battles among partners. Consider including clauses detailing the process for resolving disputes related to inventory, such as arbitration or mediation. A well-drafted agreement will minimize the risk of future conflicts and protect the interests of all partners.

Inventory Treatment in Partnership Financial Statements

Inventory is a significant asset for most partnerships and is reported on the balance sheet at its historical cost or net realizable value, whichever is lower. Historical cost represents the original purchase price of the inventory, including all associated costs like freight and handling. Net realizable value is the estimated selling price less any costs associated with selling or completing the inventory.

The choice of valuation method affects the partnership’s reported assets and profitability. The cost of goods sold (COGS), representing the cost of inventory sold during a period, is reported on the income statement and directly impacts the partnership’s net income. Accurate inventory accounting is crucial for generating reliable financial statements and making informed business decisions. Regular inventory counts and reconciliation with accounting records are necessary to ensure accuracy.

Allocation of Inventory Costs Among Partners

Fair allocation of inventory costs among partners is critical for maintaining equitable relationships. The partnership agreement should specify the method used for allocating inventory costs. Common methods include allocating costs based on each partner’s capital contribution, profit-sharing ratio, or an agreed-upon percentage. For example, if partners A and B contribute equally to the partnership, inventory costs could be split 50/50.

Alternatively, if their profit-sharing ratio is 60/40, the inventory costs could be allocated accordingly. A transparent and well-documented allocation method minimizes potential disputes and fosters trust among partners. Regular review and adjustment of the allocation method might be necessary, especially in cases of significant changes in the partnership’s operations or capital contributions.

Inventory Valuation for Tax Purposes

Inventory valuation for tax purposes is governed by specific tax regulations. Generally accepted accounting principles (GAAP) may not always align with tax regulations. The chosen method significantly impacts the partnership’s taxable income. Common methods include first-in, first-out (FIFO), last-in, first-out (LIFO), and weighted-average cost. FIFO assumes that the oldest inventory is sold first, while LIFO assumes the newest inventory is sold first.

The weighted-average cost method calculates the average cost of all inventory items. The selection of the inventory valuation method impacts the cost of goods sold and consequently the taxable income. Understanding these implications and choosing the most appropriate method based on the partnership’s specific circumstances is crucial for minimizing tax liabilities and ensuring compliance with tax regulations.

Professional tax advice is recommended to ensure proper valuation and compliance.

Technology and Inventory for the New Partnership: Business Inventory For New Bussiness Partnership

Effective inventory management is crucial for a successful business partnership, and technology plays a vital role in streamlining this process. By leveraging appropriate software and hardware, the new partnership can improve accuracy, reduce costs, and enhance overall efficiency. This section explores the technological options available and their potential benefits.

Choosing the right inventory management software is a critical step. Several options cater specifically to the needs of small businesses, offering varying levels of functionality and cost.

Inventory Management Software Options for Small Businesses

Several software packages are tailored to meet the inventory needs of small businesses. The choice depends on factors like budget, complexity of inventory, and desired features. Below is a comparison of three popular options.

| Software | Key Features | Pricing | Notes |

|---|---|---|---|

| Zoho Inventory | Order management, inventory tracking, barcode scanning integration, reporting, multi-channel sales integration | Starts at $59/month | Offers a good balance of features and affordability for small businesses. Scalable as the business grows. |

| Sortly | Visual inventory management, barcode scanning, real-time tracking, team collaboration features, reporting | Starts at $49/month | Strong visual interface, ideal for businesses with visual inventory needs. Suitable for managing assets as well as products. |

| InFlow Inventory | Comprehensive inventory management, order management, manufacturing capabilities, reporting, integrates with various platforms | Starts at $79/month | More feature-rich and expensive option, suitable for businesses with complex inventory needs and manufacturing processes. |

Benefits of Barcode Scanning and RFID Technology

Barcode scanning and Radio-Frequency Identification (RFID) technology significantly improve inventory tracking accuracy and efficiency. These technologies offer substantial advantages over manual methods.

Barcode scanning utilizes unique barcodes on each item to quickly identify and track inventory levels. This automated process reduces human error, speeds up data entry, and enables real-time inventory updates. RFID technology goes a step further by using radio waves to identify and track items without requiring line-of-sight, ideal for tracking large quantities or items in difficult-to-access locations.

For example, a retail store can use barcode scanners at the point of sale to instantly update inventory levels, while a warehouse might employ RFID tags to track pallets of goods throughout the facility, improving accuracy in stocktaking and reducing inventory discrepancies.

Integration of Inventory Management Software with Accounting Software

Integrating inventory management software with accounting software is crucial for accurate financial reporting. This integration automates data transfer between the two systems, eliminating manual data entry and reducing the risk of errors. For instance, when an item is sold through the inventory management system, the corresponding transaction is automatically recorded in the accounting software, providing a seamless flow of financial data.

This integrated approach simplifies financial reporting, improves accuracy, and saves significant time and effort. Popular accounting software such as QuickBooks and Xero often have integrations with inventory management solutions.

Optimizing Inventory Levels for Profitability

Effective inventory management is crucial for a new business partnership’s success. Optimizing inventory levels directly impacts profitability by balancing the costs of holding excess stock against the risks of stockouts and lost sales. This section details key performance indicators, forecasting methods, cost-minimization strategies, and the calculation of economic order quantity (EOQ) to achieve optimal inventory levels.

Key Performance Indicators (KPIs) for Inventory Efficiency

Several key performance indicators (KPIs) provide insights into the efficiency of inventory management. Monitoring these metrics allows businesses to identify areas for improvement and make data-driven decisions. Effective tracking ensures inventory aligns with sales projections and minimizes unnecessary holding costs.

- Inventory Turnover Ratio: This measures how efficiently inventory is sold over a specific period. A higher ratio generally indicates efficient inventory management. It is calculated as Cost of Goods Sold divided by Average Inventory.

- Days Sales of Inventory (DSI): This shows the number of days it takes to sell the average inventory. A lower DSI suggests faster inventory turnover and reduced storage costs. It’s calculated as (Average Inventory / Cost of Goods Sold)

– Number of Days. - Gross Profit Margin: While not solely an inventory metric, it reflects the profitability of sales, directly impacted by efficient inventory management. A higher gross profit margin often correlates with effective inventory control.

- Inventory Holding Cost: This represents the total cost of storing inventory, including warehousing, insurance, and obsolescence. Minimizing this cost is a key goal of efficient inventory management.

Inventory Forecasting Methods

Accurate forecasting is fundamental to maintaining optimal inventory levels. Several methods can be used, each with its own strengths and weaknesses. The choice depends on factors such as data availability, product type, and forecast horizon.

- Moving Average: This method uses the average sales of the past few periods to predict future demand. A simple moving average averages sales over a fixed number of periods; a weighted moving average assigns different weights to each period’s sales, giving more importance to recent data.

- Exponential Smoothing: This method assigns exponentially decreasing weights to older data, giving more emphasis to recent sales trends. It is particularly useful when demand is relatively stable or shows a gradual trend.

- Regression Analysis: This statistical method identifies relationships between sales and other factors (e.g., seasonality, advertising spending) to forecast future demand. It requires historical data and can be complex to implement.

For example, a retailer selling seasonal clothing might use a combination of moving average and regression analysis, incorporating seasonal factors into their forecast. A company selling staple goods might rely more heavily on exponential smoothing due to relatively stable demand.

Minimizing Storage Costs and Maximizing Shelf Space Utilization

Reducing storage costs and optimizing shelf space are critical aspects of inventory management. Strategies for achieving this include:

- Efficient Warehouse Layout: Organizing the warehouse to optimize workflow and minimize travel time for picking and packing orders. Fast-moving items should be easily accessible.

- Vertical Space Utilization: Using vertical space efficiently through racking systems and high-bay storage. This maximizes storage capacity in a limited area.

- Inventory Optimization Software: Employing software to track inventory levels in real-time, predict demand, and optimize storage space allocation.

- Negotiating Better Rates with Suppliers: Securing favorable terms with suppliers, potentially reducing storage costs by receiving smaller, more frequent deliveries.

Economic Order Quantity (EOQ) Calculation

The Economic Order Quantity (EOQ) is the optimal order size that minimizes the total inventory costs. It balances the cost of ordering with the cost of holding inventory. The formula is:

EOQ = √[(2DS)/H]

Where:* D = Annual demand

- S = Ordering cost per order

- H = Holding cost per unit per year

For example, consider a product with an annual demand (D) of 10,000 units, an ordering cost (S) of $100 per order, and a holding cost (H) of $5 per unit per year. The EOQ would be:

EOQ = √[(2

- 10,000

- 100) / 5] = 2,000 units

This indicates that ordering 2,000 units at a time would minimize the total inventory costs for this particular product. However, it’s crucial to remember that the EOQ is a simplified model and doesn’t account for factors like quantity discounts or fluctuating demand. It serves as a useful starting point for determining optimal order sizes.

Risk Management and Inventory Control

Effective inventory management is crucial for a new business partnership, but it also presents several potential risks. Ignoring these risks can significantly impact profitability and even the long-term viability of the partnership. A proactive risk management plan is therefore essential for safeguarding the inventory investment and ensuring the business’s success.Inventory control, encompassing all aspects of managing inventory levels, storage, and movement, is inherently linked to risk management.

By implementing robust procedures and strategies, the partnership can minimize potential losses and maximize the return on its inventory investment. This includes careful consideration of potential threats, developing mitigation strategies, and securing appropriate insurance coverage.

Potential Inventory Risks, Business inventory for new bussiness partnership

Several significant risks are associated with inventory management. These risks can be broadly categorized into those related to physical loss or damage, obsolescence, and financial implications. Understanding these risks allows for the development of targeted mitigation strategies.

- Obsolescence: Technology products, fashion items, and perishable goods are particularly susceptible to obsolescence. Outdated inventory becomes unsaleable, resulting in significant financial losses. For example, a tech startup might find its initial product line rendered obsolete by rapid technological advancements, leaving them with unsaleable stock.

- Damage: Physical damage to inventory can occur during storage, transportation, or handling. Improper storage conditions (e.g., extreme temperatures or humidity) can degrade the quality of goods. Accidents during shipping or mishandling in the warehouse can also cause damage. Consider the scenario of a furniture retailer experiencing damage to a shipment due to poor packaging and handling by the shipping company.

- Theft: Theft can range from small-scale pilferage by employees to large-scale organized crime. Weak security measures, inadequate inventory tracking, and lack of employee accountability can all contribute to inventory theft. A retail store, for instance, might experience significant losses due to shoplifting if security measures are insufficient.

- Spoilage/Perishability: For businesses dealing with perishable goods, spoilage is a major concern. Inadequate refrigeration, improper storage, or poor inventory rotation can lead to significant losses. A grocery store experiencing a power outage that results in the spoilage of a large quantity of perishable goods is a prime example.

Inventory Risk Mitigation Plan

A comprehensive risk mitigation plan should incorporate preventative measures, control mechanisms, and contingency plans. This plan should be reviewed and updated regularly to adapt to changing circumstances and emerging risks.

- Improved Inventory Tracking: Implementing a robust inventory management system, using barcode scanners or RFID technology, allows for accurate tracking of inventory levels, movement, and location. This minimizes the risk of theft and obsolescence.

- Enhanced Security Measures: Installing security cameras, employing security personnel, and implementing strict access controls can deter theft and vandalism. Regular security audits can identify vulnerabilities and improve security protocols.

- Optimal Storage Conditions: Maintaining appropriate storage conditions, such as temperature and humidity control, is crucial for preventing damage to goods. Regular inspections of storage areas can identify and address potential issues.

- Effective Inventory Rotation (FIFO): Implementing the First-In, First-Out (FIFO) method ensures that older inventory is used or sold before newer inventory, minimizing the risk of obsolescence and spoilage.

- Regular Inventory Audits: Conducting regular physical inventory counts and comparing them to inventory records helps identify discrepancies and potential issues such as theft or damage. This allows for timely corrective actions.

- Employee Training and Accountability: Training employees on proper inventory handling, storage, and security procedures is essential. Clear accountability measures should be in place to deter theft and negligence.

- Insurance Coverage: Securing adequate insurance coverage protects the business from significant financial losses due to theft, damage, or obsolescence.

Importance of Insurance Coverage

Insurance coverage is a critical component of any effective inventory risk management plan. It provides financial protection against unforeseen events that can cause significant inventory loss. Business interruption insurance, for instance, can cover lost profits during periods when the business is unable to operate due to inventory damage or loss. Comprehensive insurance policies, tailored to the specific needs and inventory of the partnership, should be considered.

The cost of replacing lost or damaged inventory can be substantial, and insurance can mitigate this financial burden. It’s crucial to review coverage regularly and adjust it as the business grows and its inventory changes.

Handling Damaged or Obsolete Inventory

Procedures for handling damaged or obsolete inventory should be clearly defined and consistently implemented. This includes procedures for identifying, documenting, and disposing of such inventory. Damaged goods might be repairable, salvageable for parts, or require disposal. Obsolete inventory might be sold at a discounted price, donated to charity, or recycled. Detailed documentation of the disposal process, including reasons for disposal and financial implications, is crucial for maintaining accurate inventory records and minimizing financial losses.

The process should also comply with all relevant environmental regulations regarding waste disposal.

Last Word

Establishing a robust inventory management system from the start of a new business partnership is paramount. By carefully considering the legal, financial, and operational aspects Artikeld in this guide, partners can lay a strong foundation for growth and profitability. Proactive inventory management not only minimizes risks but also optimizes resource allocation, maximizing efficiency and return on investment. Remember, a well-managed inventory is a key ingredient for a thriving business partnership.

Q&A

What are the common causes of inventory shrinkage?

Common causes include theft, damage, obsolescence, and errors in counting or recording.

How often should inventory be physically counted?

Frequency depends on the business, but at least annually, and more frequently for high-value or perishable goods.

How can we resolve disagreements between partners regarding inventory valuation?

A clearly defined inventory valuation method should be specified in the partnership agreement. If disagreements persist, seek professional accounting advice.

What insurance coverage is recommended for business inventory?

Consider comprehensive business insurance that includes coverage for theft, fire, damage, and spoilage.